Credit Card Balances Hurting Your Credit Score? Here Are 3 Quick Fixes

Credit Education , Credit Report , Credit ScoreRentReporters

November 17, 2016

6 mins read

Even with clean credit card payment histories, your credit score might be down due to the “debut usage” or “utilization” ratio.

Nothing can be more frustrating than checking your credit scores and discovering they aren’t as strong as you think they should be, even though you pay your bills on time. For those with clean payment histories, the culprit bringing down their scores is often a formula that sounds like it was created by an evil mathematician: the “debt usage” or “utilization” ratio.

If that term dredges up bad memories of high school algebra class, relax. We’ll break it down and make both the problem—and the fixes—clear.

What’s the Problem?

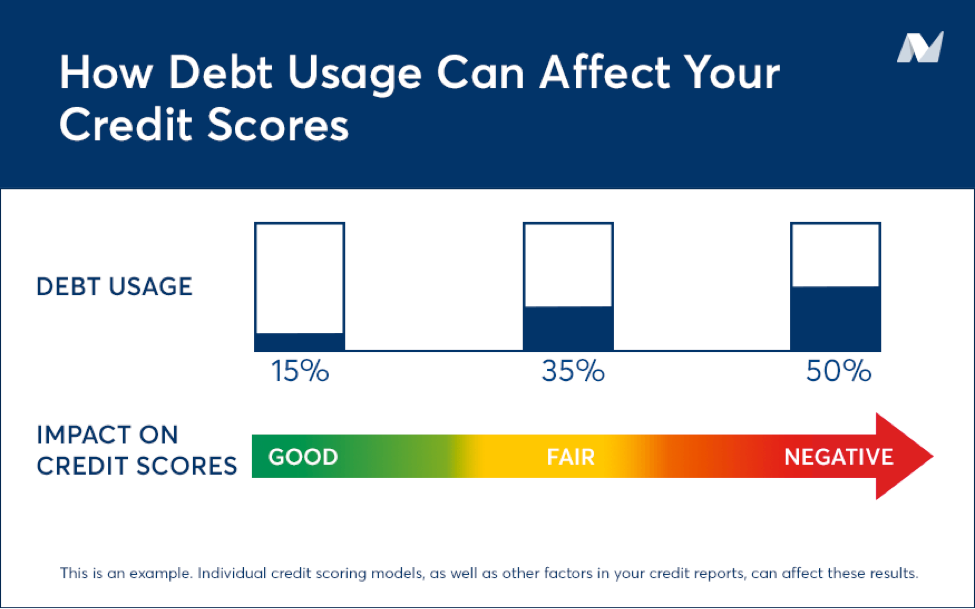

Your “debt usage” ratio or “utilization ratio” compares your balances on your revolving accounts, like credit cards, to your credit limits. High balances relative to your credit limits hurt your scores, while low balances can help. Most credit scoring models will look at debt usage on each revolving account, as well as all of them together. That means large amounts of available credit can be beneficial to your credit scores.

Why Paying in Full Isn’t A Fix

What if you pay off your balance each month? Unfortunately, debt usage can hurt you just like it can affect those who carry balances. Why? Because most card issuers report account balances to the credit bureaus before your payments are due (and received).

In fact, most issuers send account information to the credit bureaus at the end of the billing cycle; the time each month when the issuer tallies up what you owe, sends you a bill, and usually gives you the option of paying it off or making minimum payments. The credit bureaus don’t get an update when you subsequently make your payment. And that means you aren’t getting “credit,” so to speak, for paying in full.

The Formula

To calculate your debt usage ratio, grab your calculator and divide the balance by the credit limit, then move the decimal two places to the right.

For example:

$350 balance/$1,000 credit limit

350 / 1,000 = .35 or 35% debt usage

How Low Must You Go?

You may have heard the ideal utilization ratio is below 50%…or 30%…or some other number. But credit scores are much more complex than that and the exact formulas are kept under wraps.

Here’s what we do know: FICO does say that consumers with the highest credit scores, on average, maintain debt usage ratios below 10%. But if that seems impossibly low, don’t panic. Most people can get away with a debt usage ratio of 20% to 25% before it starts to affect their scores, provided other credit score factors (like payment history, for example) are strong.

What You Can Do!

Here are three ways to reduce your debt usage ratio and improve your credit scores:

- Pay faster

As mentioned earlier, most credit card issuers report balances around the time the billing cycle closes. (You can check your free annual credit reports to confirm when your issuers report.) If your payment is posted to your account before that date, you’ll reduce the balance that appears on your credit reports. You can usually accomplish this by making an online payment on your account a few days before the due date. (If you are trying to avoid interest, always double check to make sure you pay off the previous statement balance before the due date.)

- Pay More

If you’ve been consistently carrying high balances on your credit cards, look for ways to pay them down more quickly. Hold a garage sale and use the proceeds to pay down the card with the highest balance in comparison to the credit limit. Or pick up extra income as an Uber driver or in some other side gig, and use that to chip away at a balance.

- Consolidate

While all debt can affect your credit scores, installment loans—loans for a fixed amount—aren’t affected by the debt usage ratio the way credit cards are. That means you can consolidate your credit card debt with a personal loan, and by doing so, you may improve your scores. Just don’t close the credit card accounts you’ve just paid off or you’ll reduce your overall credit limits, which may then wipe out the benefit of reducing those balances.

The good news? If this credit score factor is bringing down your scores, improving it can often provide a quick fix. We’ve seen scores rise by 10 to 40 points or more in a single month because of the strategies here. Credit scores are calculated based on the information in your reports at the time the score is requested, so as soon as your issuer reports your lower balances, the sooner you’ll see results.

Written by Gerri Detweiler, author of five books, including her newest title, Finance Your Own Business: Get On The Financing Fast Track, coauthored with best-selling author and corporate attorney Garrett Sutton; and the free ebook Debt Collection Answers: How to Use Debt Collection Laws to Protect Your Rights. Gerri is also a frequent contributor to credit.com